The Breakeven Point: How We Stress-Test Our 2026 Financial Models

In a “up-only” market, underwriting is easy. You plug in 5% rent growth, 3% expense inflation, and a compressed exit cap, and every deal looks like a home run.

But Altos Holdings wasn’t built for “up-only” markets. We build our models for the “What Ifs.” What if the local employer moves? What if insurance premiums double again? What if interest rates don’t move for another 24 months?

Before we ever issue an LOI, we subject every deal to a three-tier Multifamily Stress Test. Here is how we find the “breaking point” of an asset.

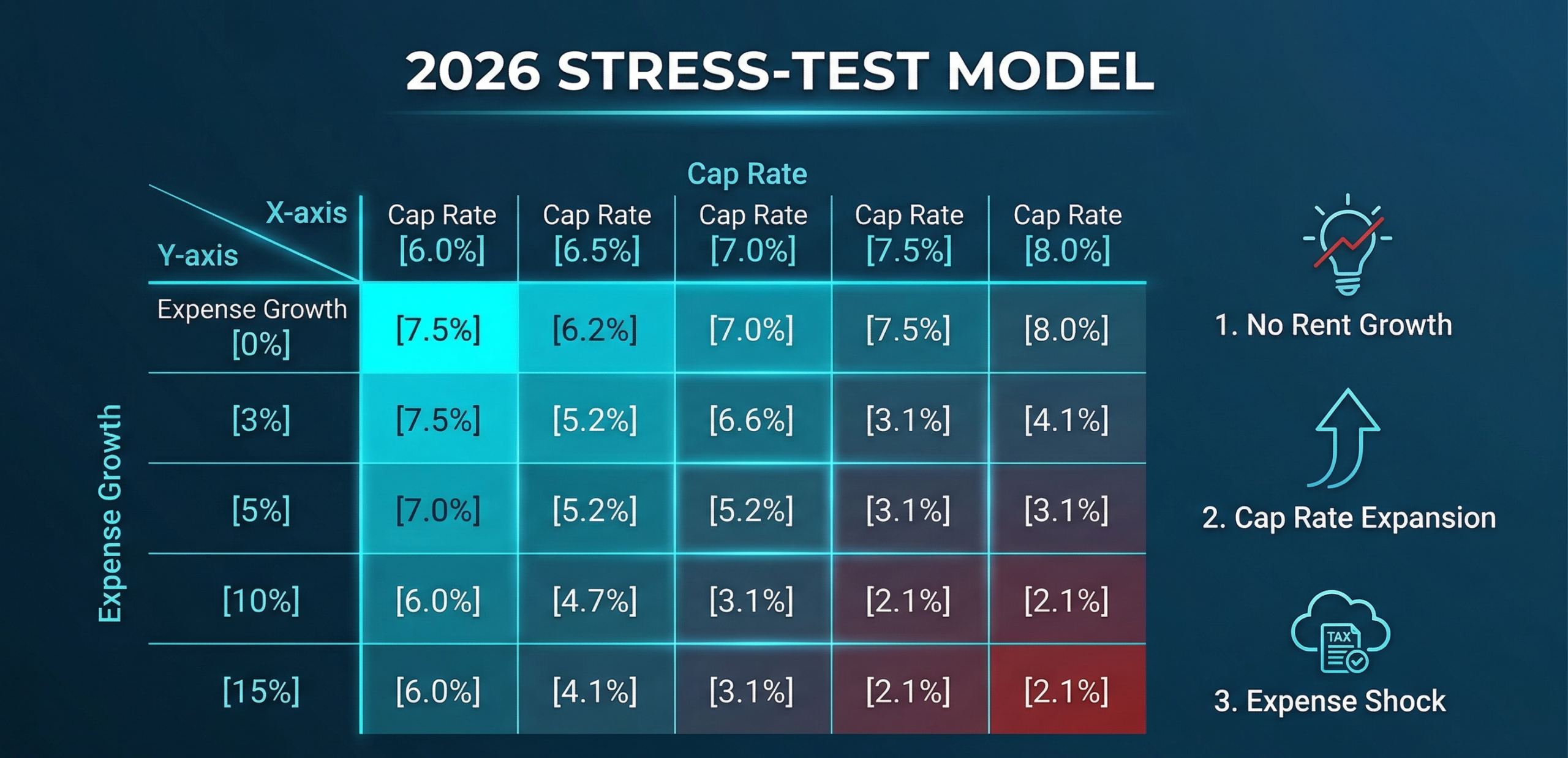

1. The “Stagnant Rent” Test

The biggest lie in many broker OMs right now is the “Year 1 Rent Pop.” They assume you can buy a building and immediately raise every tenant by $200.

- Our Test: We run the model with 0% rent growth for the first 24 months.

- The Goal: The property must still maintain a Debt Service Coverage Ratio (DSCR) of 1.25x or higher without a single dollar of rent increases. If the deal requires immediate “pops” just to pay the mortgage, we pass.

2. The Expense Shock (Insurance & Taxes)

In 2026, the two “silent killers” of NOI are property taxes and insurance. We’ve seen premiums in some corridors jump significantly in a single year.

- The External Data: With the HUD 2026 Operating Cost Adjustment Factors (OCAF) projecting a 5.1% national average increase in expenses, our 10%–15% “Shock” test ensures we remain well ahead of the inflationary curve.

- The Altos Rule: We model a 20% “Shock Increase” to insurance and a full tax reassessment at the purchase price. We want to ensure that even if expenses outpace inflation, the cash-on-cash return remains positive.

3. Our Rigorous Multifamily Stress Test for Exit Caps

This is where most syndicators get burned. They assume they will sell the building at the same “Cap Rate” they bought it at—or lower.

- Our Test: We add 50 to 100 basis points (0.5% – 1.0%) to the exit cap rate. If we buy at a 6% cap, we model the sale at a 7% cap.

- The Internal Strategy: Our stress-testing parameters are updated quarterly based on the macro data found in our 2026 Investment Thesis. We don’t rely on the market getting “better” to make our money; we rely on the forced appreciation we create through disciplined operations.

Why This Matters to Our Partners

When we say we’ve stress-tested a model, we mean we’ve tried to break it. We aren’t looking for the deal that looks best on a sunny day; we are looking for the deal that stays dry when it pours. By the time an investment reaches our partners, it has already survived the “Altos Gauntlet.