In my previous deep-dive into the Altos Holdings 2026 Moat Underwriting Strategy, I laid out our defensive framework for navigating a volatile Florida market. Today, we are moving from theory to high-stakes execution by targeting a broken capital stack multifamily opportunity in the heart of Orlando.

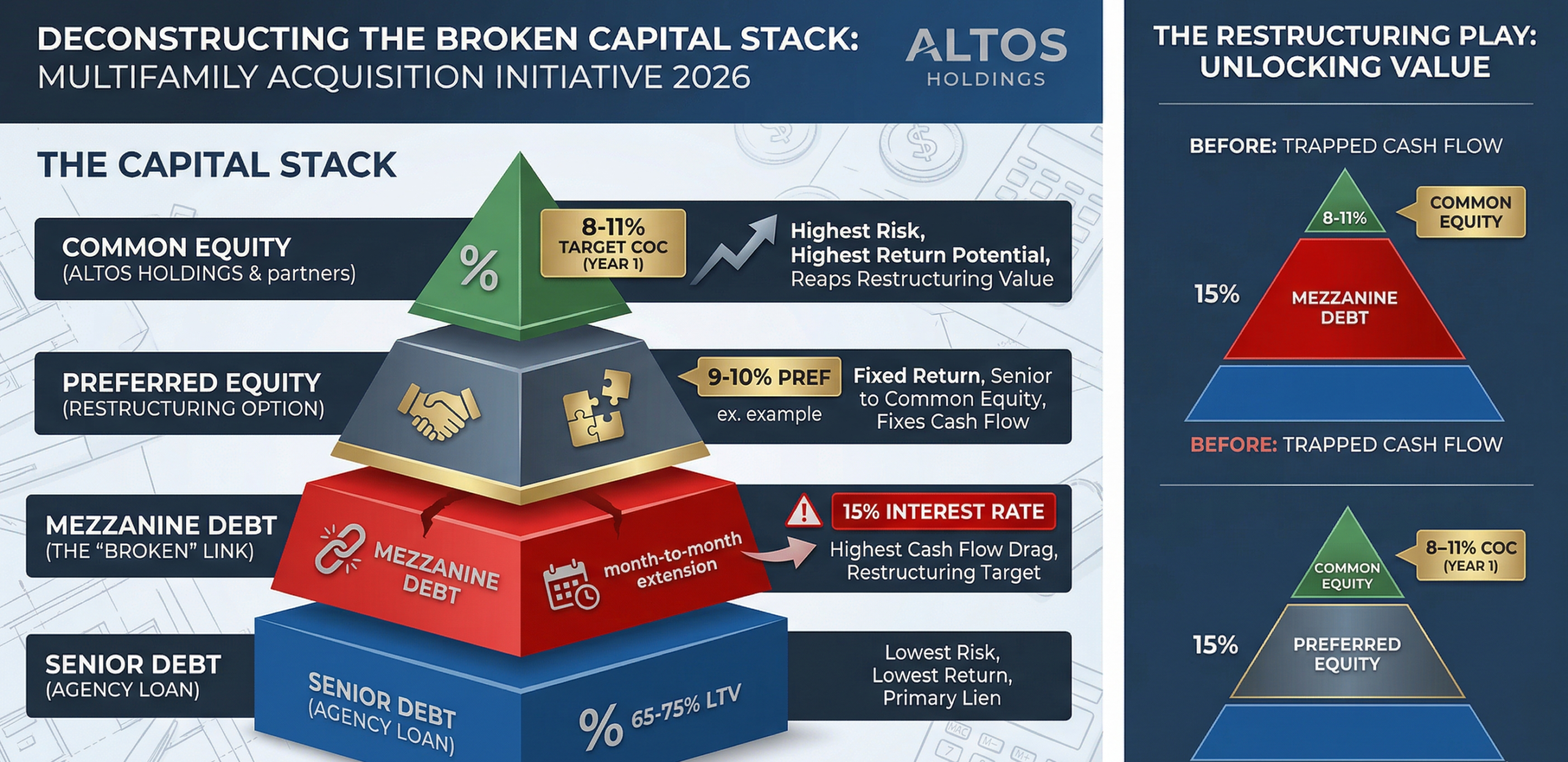

The Anatomy of a Broken Capital Stack Multifamily Deal

While general investors are sidelined by high interest rates, we are hunting for specific financial distress. At Altos Holdings, we aren’t looking for “broken buildings”—we are looking for broken balance sheets. Consequently, our focus shifts toward institutional-quality assets that are simply weighed down by inefficient debt.

The Esplanade Apartments deal serves as a perfect case study for this approach. This 186-unit, 2009-vintage asset is a premier concrete-slab build currently trapped in a predatory debt structure. Specifically, the current owner is managing a bridge loan on a month-to-month extension alongside a $7.0M mezzanine loan with a 15% interest rate.

In a market where organic rent growth has flattened—as noted in the latest Northmarq market fundamentals report—this 15% debt is a silent killer. Therefore, this is exactly where our broken capital stack multifamily expertise creates a significant competitive advantage for our partners.

Why This Broken Capital Stack Multifamily Deal Fits the Altos “Moat”

Many buyers see the term “mezzanine debt” and walk away immediately. However, we see a clear path to an 8.1% Year 1 Cash-on-Cash return. Here is how we stress-tested this broken capital stack multifamily asset:

1. The 0% Rent Growth Stress Test

First, our underwriting models flat rent for 2026. Even without a market miracle, the property generates healthy cash flow because the 2009 build is exempt from the “insurance tax” currently killing older 1970s assets. Furthermore, the concrete construction provides a long-term durability moat.

2. The Debt Restructuring Arbitrage

In addition to physical durability, we focus on financial engineering. By replacing the 15% mezzanine “broken link” with fresh equity or cheaper capital, we unlock the property’s Net Operating Income (NOI). Because 168 of 186 units are already renovated, we aren’t taking on construction risk; instead, we are simply fixing the math.

3. Safety of Basis and Appraisal Alignment

Finally, we are entering at a purchase price of $37M ($198,925/door). This represents a disciplined entry point compared to the $36.4M Agency appraisal. As a result, we provide a vital safety buffer for our equity partners from day one.

Unlocking Value in a Flat Market

This broken capital stack multifamily strategy allows us to acquire institutional-quality assets without paying a “premium” for market timing. By buying durability and fixing the capital stack, we aim to ensure a 35.3% 5-year levered IRR.

Acquisitions Note: Is your property trapped in a month-to-month bridge extension? Altos Holdings specializes in broken capital stack multifamily recapitalization.